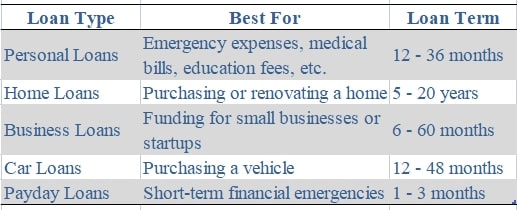

1. Types of Loans You Can Apply For

Before diving into the application process, it's crucial to understand the different types of loans available. Here's an overview of the most common loan types and what they are best suited for:

2. How to Apply for a Loan: The Step-by-Step Process

Once you've decided what type of loan you need, it’s time to understand the application process. Here’s a simple step-by-step breakdown to make the journey easy for you.

Step 1: Determine the Loan You Need

Before you apply, identify your needs. Do you need a personal loan to cover unexpected medical bills or want a business loan to expand your business? Knowing what type of loan you need will help narrow down your choices.

Step 2: Check Your Eligibility

Lenders have specific requirements depending on the loan type. Common eligibility criteria include:

- Age: Applicants are usually required to be at least 21 years old.

- Income: Lenders will want to ensure you have a steady source of income.

- Credit Score: A good credit score can help you secure better terms, though many lenders offer loans to individuals with varied credit histories.

- Documents: Proof of identity, proof of income, and sometimes proof of residence are standard documents required.

Step 3: Compare Lenders and Loan Terms

Once you’ve determined your eligibility, it’s time to shop around. Compare loan options from different lenders, including:

- Banks: Traditional financial institutions such as BDO, Citibank, and Chase offer competitive loan products.

- Online Lenders: Lenders like Tala, Cashalo, or other online platforms often provide faster approval with more flexible eligibility criteria.

- Microfinance Institutions: If you're looking for smaller loan amounts, microfinance institutions can be an excellent option for quick, small loans.

When comparing, pay attention to:

- Interest Rates: Lower rates usually mean you’ll pay less over time.

- Loan Amount: Only borrow what you need. Larger loans come with larger repayment obligations.

- Repayment Terms: Make sure the repayment period aligns with your financial situation.

Step 4: Submit Your Loan Application

Once you’ve selected a lender, it’s time to apply. Most lenders will ask for:

- A completed application form.

- Proof of identity and income (pay slips, tax returns, etc.).

- Other documents as required (such as utility bills or business registration).

The application process can often be done online or at a local branch, depending on the lender.

Step 5: Wait for Approval

After submitting your application, the lender will process it. The time it takes to approve a loan varies. In some cases, approval can be as quick as a few hours, while others may take a few days. Once approved, the lender will inform you of the loan terms, including the amount, interest rate, and repayment schedule.

Step 6: Sign the Loan Agreement

Once you agree to the terms, the final step is signing the loan agreement. This legally formalizes the loan and outlines both your rights and responsibilities as a borrower. Read the contract carefully to ensure everything is as discussed.

3. Factors to Consider When Choosing a Loan

When applying for a loan, there are several key factors to keep in mind:

-

Interest Rates: Lower interest rates result in lower monthly payments and less paid over the loan's duration. Always shop for the best rate.

-

Loan Amount: Don’t borrow more than necessary. Only borrow what you need to avoid higher monthly payments and unnecessary debt.

-

Repayment Terms: Make sure the terms suit your financial situation. For example, longer repayment terms generally mean smaller payments but may result in paying more in interest.

-

Lender Reputation: Choose a reputable lender with transparent processes and positive reviews. Avoid lenders with hidden fees or unclear loan terms.

-

Fees and Charges: Look out for any hidden fees, such as processing fees or early repayment charges, that could add to the total loan cost.

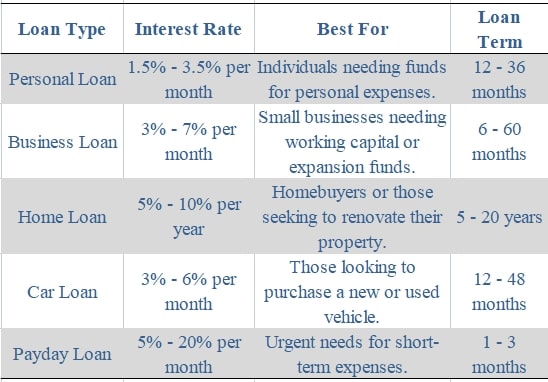

4. Common Loan Options to Consider

Here are some of the most common loans you might apply for:

Conclusion: Ready to Apply for a Loan?

Now that you understand the loan application process and have all the necessary information, you’re ready to take the next step. Remember to compare different lenders and terms to find the loan that best fits your needs.

By following this guide, you can confidently apply for a loan and secure the funds you need to achieve your goals—whether personal or business-related. Always make sure to choose a reputable lender, understand your repayment obligations, and stay within your borrowing limits.

With careful planning and the right loan, you’ll be on your way to financial success!